Brookings Institution Highlights Stablecoin Implications For US Treasuries In New Report

Stablecoins are no longer a niche crypto instrument; they have become a structural force in global finance.

Stablecoins are no longer a niche crypto instrument; they have become a structural force in global finance.

That is the conclusion of a new Brookings Institution working paper published this month, titled “The Rise of Stablecoins and Implications for Treasury Markets”. The report finds that as stablecoins gain traction in cross-border payments and remittance corridors, issuers such as Tether and Circle are emerging as major holders of short-term U.S. Treasury bills. Together, their portfolios now rival those of some foreign governments.

Brookings’ analysis goes beyond market snapshots. It explores how this new source of demand is reshaping Treasury liquidity, fiscal resilience, and even the geographic footprint of dollar circulation. Stablecoins, once seen as a crypto-native convenience, now directly influence the cost of U.S. government borrowing and the global flow of capital.

More broadly, stablecoins are becoming the connective tissue between on-chain and traditional markets. Understanding their interaction with the Treasury system is essential to designing the next generation of compliant, yield-generating products.

Adoption Drivers and Market Map

Stablecoins continue to spread across borders for one simple reason: they make money move faster, cheaper, and with fewer barriers than the traditional banking system.

In many remittance corridors, they have already replaced wire transfers as the preferred way to send dollars abroad. For users in countries facing inflation or currency depreciation, stablecoins offer a familiar store of value and an accessible digital payment tool that does not rely on local banks.

Brookings identifies these efficiency gains in speed, cost reduction, and transparency as the primary catalysts for growth. Policy momentum has also accelerated adoption. The Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act of 2024 created the first unified federal framework for dollar-pegged stablecoins. It requires issuers to maintain 100% reserves in cash, short-term Treasury bills, and other approved assets, effectively tying the expansion of stablecoins to U.S. government debt issuance.

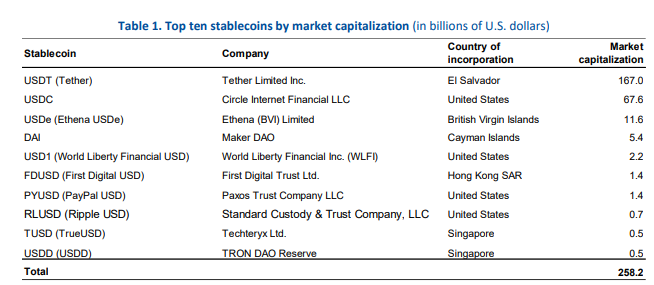

This combination of regulatory clarity and real-world utility has driven the stablecoin market to more than $250 billion in capitalization, led by USDT ($167 billion) and USDC ($68 billion). More than 80% of stablecoin transactions now occur outside the United States, with the highest adoption seen in regions such as sub-Saharan Africa and Southeast Asia. In these markets, stablecoins are not speculative assets; they are working capital for businesses, remittance tools for families, and increasingly, financial infrastructure for entire economies.

Stablecoins have evolved from a crypto payment novelty into a globally distributed dollar network. Each new transaction, wallet, and merchant using them adds weight to their influence on real-world liquidity and on the short-term Treasury market that backs them.

Stablecoins as a Structural Bid for T-Bills

As stablecoins expand globally, their issuers have become major participants in the short-term U.S. Treasury market. According to Brookings, more than 80% of the reserves held by leading stablecoins such as USDT and USDC are now invested in short-dated Treasury securities.

By mid-2025, their combined exposure exceeded $177 billion, representing about 0.6% of all outstanding Treasuries.

Tether alone holds a share comparable to that of entire countries, ranking alongside Germany and the United Arab Emirates in foreign Treasury holdings. If this growth continues, stablecoin issuers could soon rival traditional foreign investors in financing the U.S. government’s short-term debt. The report finds that between late 2023 and late 2024, Tether accounted for roughly 4.6% of new foreign purchases of Treasury securities, which is on a scale once reserved for sovereign funds and central banks.

This structural demand is not a one-time phenomenon. As dollar-backed stablecoins grow in circulation, issuers must continually purchase new Treasury bills to match their outstanding supply. Each token effectively represents a claim on a short-term government bond, linking the pace of stablecoin adoption directly to Treasury market demand.

Brookings projects that under reasonable global growth and adoption scenarios, total stablecoin market capitalization could exceed $2 trillion by 2030. Most of that value would likely be backed by U.S. Treasury bills, cementing stablecoins as a permanent fixture of government debt markets. In practice, this means that every uptick in cross-border stablecoin use reinforces demand for Treasuries, creating a feedback loop between digital dollars and the fiscal machinery of the United States.

Implications and Institutional Perspective

Brookings frames the rise of stablecoins as a fiscal opportunity and a financial stability challenge.

On one hand, stablecoins diversify the investor base for U.S. Treasury bills and expand retail exposure to government debt through intermediaries such as Tether and Circle. This added demand helps lower short-term borrowing costs and broadens participation in U.S. debt markets. By lowering average interest expenses, even small shifts in yield can translate into significant fiscal savings — an, estimated $37 billion in reduced annual interest payments for every 10 basis point decline.

The other side of the equation is risk. A market increasingly reliant on a few private issuers for Treasury demand could become sensitive to crypto-related volatility. Outflows from stablecoins can trigger liquidity shocks, forcing issuers to sell Treasury holdings and pushing yields upward. Brookings notes that outflows have roughly two to three times the yield impact of inflows, underscoring how quickly stablecoin redemptions can influence short-term funding markets.

The report also highlights broader systemic concerns. Concentration among a handful of issuers introduces “too big to fail” dynamics, while the rapid spread of stablecoins in developing economies raises questions about local currency substitution and monetary control. For regulators, this calls for coordinated global oversight, enhanced reserve transparency, and robust stress testing for stablecoin issuers.

From our perspective, these dynamics reinforce the importance of building tokenized financial infrastructure that is transparent, risk-aware, and policy-aligned. The goal is to capture the efficiency gains of on-chain liquidity without inheriting the fragility of unregulated markets. Our On-Chain Traded Fund (OTF) products are designed with these principles in mind, enabling institutional partners to access yield backed by real, verifiable assets while preserving redemption reliability and regulatory compliance.

For builders and institutions, this shift signals a new era of integration between digital and traditional finance. Stablecoins are no longer peripheral instruments; they are now part of the plumbing of global liquidity. The challenge ahead lies in ensuring that this new layer of the financial system is governed with the same prudence and transparency that support the markets it now helps sustain.

Bridging Fiscal Infrastructure and On-Chain Innovation

Brookings’ analysis captures a moment when stablecoins have crossed from being crypto’s liquidity backbone into a structural, impossible-to-ignore participant in the U.S. Treasury market, potentially significantly influencing liquidity, yields, and even the balance of global capital flows.

For policymakers, the path forward requires balancing efficiency with resilience. Stablecoins have proven their ability to improve cross-border payments and broaden access to the dollar, but their rapid growth also ties crypto markets more closely to sovereign debt systems. Clear reserve standards, coordinated regulation, and transparent reporting will be essential to safeguard both sides of this relationship.

As stablecoins integrate more deeply with traditional finance, the need for secure, compliant infrastructure becomes paramount. We’ll work to help institutions participate in this next phase of on-chain finance with confidence through products that preserve liquidity, uphold transparency, and align with the evolving policy landscape.