How Stablecoins Could Lower U.S. Interest Rates

A new conversation is emerging from inside the Federal Reserve: stablecoins could eventually influence U.S. interest rates and create a…

A new conversation is emerging from inside the Federal Reserve: stablecoins could eventually influence U.S. interest rates and create a more favorable economic environment for the nation.

The argument, articulated most clearly by Fed Governor Stephen Miran in a recent speech at the Harvard Club of New York City on November 7th, is that the rise of stablecoins may exert persistent downward pressure on the neutral rate of interest, which is the level that keeps the economy in balance when inflation is stable and growth is steady.

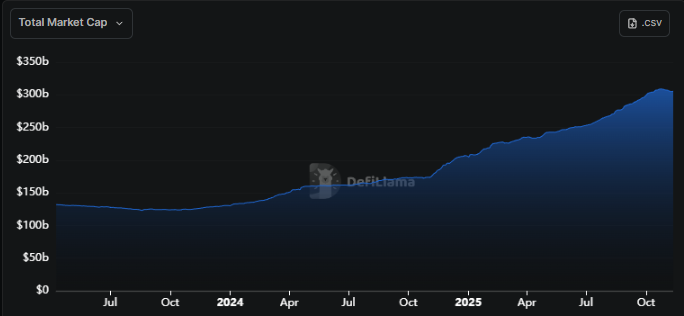

Under the recently enacted GENIUS Act, stablecoin issuers in the United States must back every token with safe, dollar-denominated assets such as Treasury bills, repurchase agreements, or money market funds. As global demand for these tokens grows, issuers are required to purchase more of those instruments, creating steady, incremental demand for U.S. government debt.

It’s pretty straightforward: more stablecoin demand means more stablecoin issuance, more issuance means more buyers of Treasurys, and more buyers of Treasurys means higher prices and lower yields. It could also be inferred that lower Treasury yields would increase demand for the high yields that can be earned today by holding today’s stablecoins, looping the end of the demand channel to the start, forming a flywheel.

Miran’s analysis suggests that the scale of stablecoin issuance expected by the end of this decade, potentially one to three trillion dollars, could meaningfully influence how cheap or expensive it is for the U.S. government to borrow.

In effect, the world’s appetite for digital dollars may become a new determinant of the nation’s cost of capital, effectively linking the entire global economy to on-chain markets.

A New Source Of Treasury Demand

The GENIUS Act formalized what had already become common practice among major stablecoin issuers: holding reserves in short-term, dollar-denominated instruments that carry minimal risk. By law, U.S.-regulated issuers must now maintain one-to-one backing with assets such as Treasury bills, overnight repos, or government money market funds.

This mechanism turns global stablecoin demand into a new pipeline of foreign capital entering the U.S. financial system. When users in emerging markets or overseas businesses acquire dollar-backed stablecoins, the issuers behind those tokens must acquire matching Treasury assets to maintain their peg. The result is a continuous flow of international savings into U.S. Treasurys.

If stablecoin adoption grows to the projected one to three trillion dollars by the end of the decade, the implications are substantial. That level of issuance would create Treasury demand on par with major rounds of quantitative easing, except that it would be driven by market activity rather than central bank policy. In Miran’s framework, this additional and relatively price-insensitive demand lowers yields across the curve and compresses funding costs for both the public and private sectors.

The r* Effect: A Global Stablecoin Glut

At the center of Miran’s thesis is the neutral rate of interest, known as r*. It represents the rate that keeps the economy steady when inflation is stable and output is at potential.

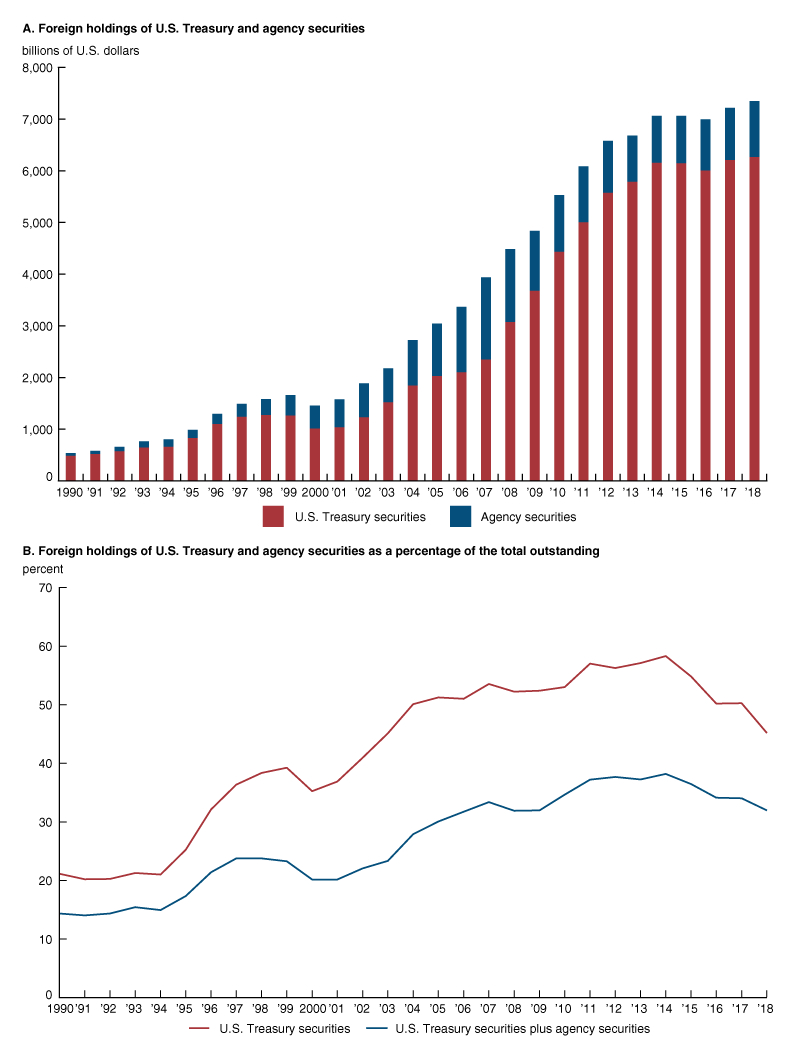

If stablecoin adoption increases the supply of loanable funds in the U.S. economy, the equilibrium rate that balances saving and investment moves lower. That dynamic mirrors what former Fed Chair Ben Bernanke once described as the “global savings glut” of the early 2000s, when an influx of foreign capital into U.S. assets depressed yields for years.

Stablecoins could now create a similar version of that phenomenon. Every dollar of stablecoin reserves backed by Treasurys expands the pool of funds available for lending and investment. As the market for these tokens grows, it raises steady, non-cyclical demand for short-term government debt and other highly liquid assets. The outcome should be a gradual, structural downward shift in yields that influences how the Fed interprets neutral policy settings.

Early research (2024) estimates that widespread stablecoin use, if fully backed by U.S. securities, could lower interest rates by as much as 40 basis points, Miran shared in his speech. Even moderate growth, roughly two to four trillion dollars in reserves, could amount to thirty to sixty percent of the rate impact once attributed to the global savings glut.

For an economy the size of the United States, that is not a marginal adjustment. It changes how the central bank calibrates policy, how capital markets price risk, and how long-term borrowing costs evolve.

If Miran’s view proves correct, the scaling of stablecoin reserves could lead to a future where neutral interest rates settle lower than most policymakers currently anticipate, providing easier financing conditions for governments and corporations. And with the international AI arms race ongoing, this shift could prove to be incredibly advantageous and well-timed to support the U.S.’s efforts to lead the industry. In that regard, it’s in the government’s best interest to support the growth of dollar-backed stablecoins as much as possible

Expanding The Lifespan & Reach Of The Dollar

Stablecoins have the potential to extend the reach of the U.S. dollar in a way that traditional banking systems have struggled to achieve in recent years. By operating on open, borderless networks, they make dollar access possible for individuals and institutions in regions where capital controls, weak banking infrastructure, or volatile local currencies limit financial stability. Each dollar-backed token represents a bridge between foreign demand for financial security and the liquidity of U.S. capital markets.

This flow of capital from emerging markets into digital dollars effectively exports U.S. monetary policy and establishes more free market control over it.

Savers in countries facing inflation or currency depreciation can hold assets tied to the Federal Reserve’s balance sheet rather than their own central bank’s, creating a behind-the-scenes, but powerful form of digital dollarization that reinforces the dollar’s dominance as the preferred global store of value while binding more of the world’s liquidity to the performance of U.S. financial markets.

Most importantly, a lower neutral rate would enable the U.S. economy to sustain growth at lower interest rates than before, representing a profound turning point for the nation as international competition in AI, weapons manufacturing, robotics, and other key sectors intensifies year over year.