Research: An Analysis Of Yield-Bearing Stablecoins

Following the expansion of stablecoin-based yield products, our research team has observed a growing wave of structured stablecoin and…

Following the expansion of stablecoin-based yield products, our research team has observed a growing wave of structured stablecoin and credit-focused protocols emerging across the industry. These projects combine on-chain and off-chain credit underwriting, delta-neutral trading, real-world asset exposure, and DeFi-native vault strategies to offer an enhanced yield on stablecoin deposits.

In this report, we compile a summary of several notable projects pursuing these models, outlining their positioning, product structures, risk frameworks, and yield mechanics.

3jane

Positioning

3Jane is an unsecured lending protocol positioned similarly to Maple Finance prior to 2022. While Maple focused exclusively on institutional borrowers, 3Jane expands its target market to include both U.S. institutions and retail users.

The protocol supports on-chain collateral but is designed to go beyond traditional crypto-native risk models. It can incorporate off-chain data such as bank-held assets, projected future cash flows, and borrower credit scores into its underwriting process, enabling more flexible and comprehensive credit assessments.

3Jane is backed by Paradigm and Coinbase Ventures and has disclosed $5.2 million in funding to date. On the product side, the protocol offers a stablecoin deposit structure where users deposit USDC and receive USD3 or sUSD3 in return.

Flow

Users deposit USDC to mint USD3, and those funds are allocated into a shared lending pool. The pool then lends USDC to approved borrowers. Borrowers pay interest on these loans, and that interest is generated from the lending activity within the pool.

Deposit side

On the deposit side, USD3 and sUSD3 function as tranches within a shared credit pool. Users deposit USDC and receive either USD3 or sUSD3 in return. USD3 represents the senior tranche and offers standard, more stable yield, while sUSD3 represents the junior tranche and is designed to provide higher yield in exchange for greater risk.

Pool

Capital is lent out via 3Jane’s credit engine to eligible borrowers (only US citizens are available )

Borrower side

On the borrower side, users can access unsecured loans based on a combination of data sources, including their centralized exchange account activity, on-chain wallet history, off-chain bank assets, and traditional credit scores. Borrowers pay interest on these loans, and the interest income is distributed between USD3 and sUSD3 holders according to the risk structure of their respective tranches.

USD3 vs sUSD3: risk tranching

USD3 — senior tranche

USD3 represents the senior tranche. Its primary goal is safety. During the current bootstrapping phase, USD3 operates in a fully risk-off configuration, where funds are only deposited into Aave’s USDC market. All interest earned from Aave is directed to sUSD3 holders, not USD3 holders. Instead, USD3 holders primarily receive JANE token incentives. So far, 7 million JANE tokens have been emitted, and there is currently no secondary market liquidity for the token. The yield for USD3 is relatively low and largely driven by JANE incentives, but there is effectively no credit risk during this phase. Conceptually, USD3 can be viewed as a low-risk position whose upside comes from the expected future value of JANE and potential TGE-related incentives.

sUSD3 — junior tranche

sUSD3 represents the junior tranche and is capped at 15% of the total pool. It has an unlock or cooldown period that applies before tokens can be redeemed. In the event of borrower defaults, sUSD3 is the first tranche to absorb losses. The yield for sUSD3 includes both the Aave USDC interest generated from the USD3 collateral and the credit yield from unsecured loans made to borrowers. This structure results in much higher potential returns, but also significantly higher risk. The current APY is around 27%. Conceptually, sUSD3 can be viewed as a leveraged, high-risk position that captures the full credit spread from borrower activity.

Other Info

USD3 has opened two deposit tranches:

- First tranche: $25m cap, fully filled on Nov 18.

- Second tranche: $12.5m cap, still ongoing.

On Pendle there is currently a pool for USD3. The YT implied yield is 15.5%, which you can loosely interpret as the market’s implied expectation for the JANE emissions yield.

However, the pool’s TVL is quite small (less than $1m) — a $2k trade in YT can move the price by ~10%, so it’s not a very reliable reference.

Almanak

Almanak positions itself as an AI-driven DeFi platform that functions like an on-chain fund, where the role of the curator is handled by an AI agent. Rather than relying on human-managed strategies, the platform uses AI to design fully on-chain DeFi strategies and packages them into vault products that users can access directly.

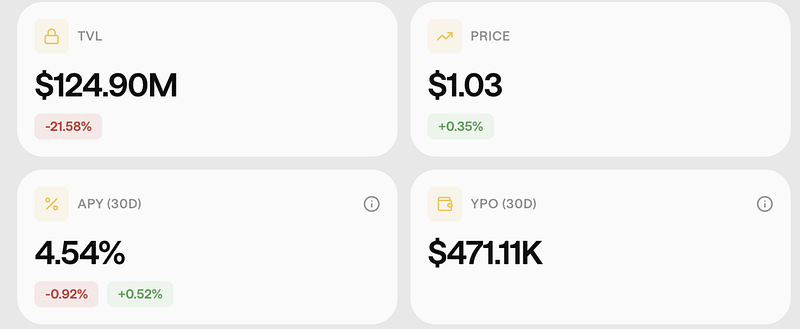

On the stablecoin deposit side, Almanak offers the alUSD Vault. Users deposit USDC and other supported stablecoins into these vaults and receive alUSD vault share tokens in return. The alUSD product has grown to around $140 million in total value locked, with an APY of roughly 5%, positioning it as a lower-risk, yield-generating stablecoin strategy.

Other Info

Almanak is preparing for an ICO on Legion at a $90 million valuation, with vesting applied to the token distribution. In parallel, Pendle YT exposure has been framed as an alternative way to gain economic exposure ahead of the launch.

Based on Almanak’s own points and incentives calculations, purchasing YT at current rates is presented as being roughly equivalent to acquiring the token at an effective valuation of around $120 million, assuming those incentive models and assumptions ultimately hold.

Neutrl

Neutrl positions itself as a delta-neutral stablecoin protocol, but unlike most basis trading platforms that focus primarily on BTC and ETH, it concentrates on altcoins, especially newer and less liquid tokens. The strategy involves acquiring discounted tokens through OTC deals with foundations, whales, and market makers, including locked or vesting allocations, and then hedging exposure through perpetual futures or pre-listing markets.

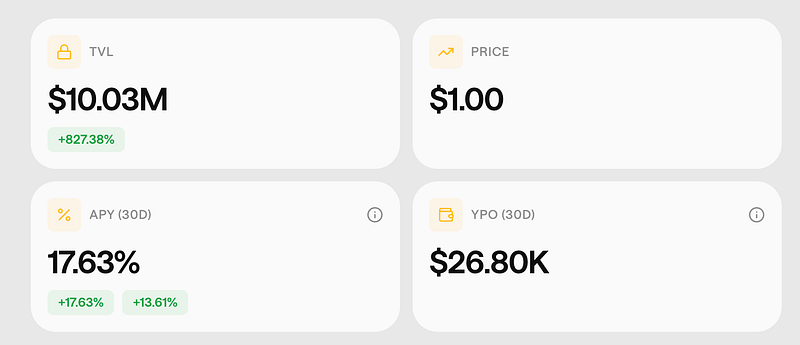

The project has disclosed $5 million in funding and operates a dual-token structure composed of NUSD and sNUSD. Capital has been raised through two capped deposit rounds, with the first capped at $75 million and the second capped at $50 million, bringing total current TVL to $125 million.

The recent APY for sNUSD is approximately 17.63%. If the strategy were limited to BTC and ETH delta-neutral trades, expected yields would likely be closer to those seen in products like USDe. The elevated yield is largely driven by Neutrl’s exposure to altcoin basis and pre-listing market inefficiencies.

Risks

The primary risk in Neutrl’s strategy stems from its emphasis on newer and less liquid tokens. Because many of its hedged positions involve illiquid or pre-listing assets, there is a non-trivial risk of short squeezes, where rapid price moves can overwhelm hedges and force losses.

Most delta-neutral protocols concentrate on BTC, ETH, or other highly liquid assets to minimize these risks. Neutrl’s focus on altcoins increases both basis risk and liquidity risk, making its return profile more volatile and more sensitive to market dislocations.

Reflect

Reflect is a Solana-based stablecoin protocol backed by a16z. Its main strategy is to deploy user-deposited USDC across multiple Solana-based lending and perpetuals protocols, including Drift, MarginFi, and Kamino.

User funds are routed into these protocols to generate yield, and the performance of Reflect’s USDC+ product is roughly in line with Kamino’s USDC vault yield, reflecting the strategy’s close alignment with existing Solana money market and perp ecosystem returns.

Nest

Nest is an RWA-focused vault protocol built on Plume that follows a Midas-style model. Users deposit stablecoins into the protocol, and those funds are deployed by vaults into tokenized real world assets, including credit and private credit exposures.

In return, users receive vault share tokens such as nCREDIT, which represent their proportional claim on the underlying RWA-backed vault.

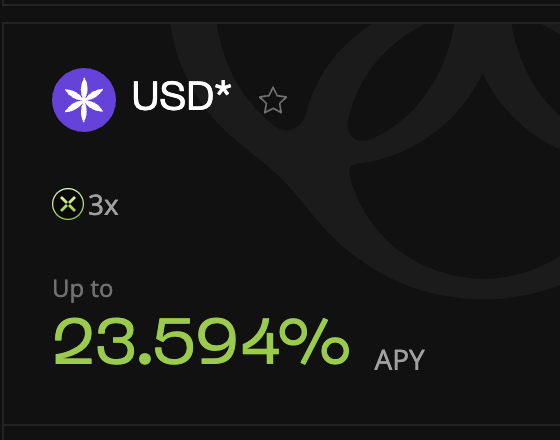

Perena

Perena positions itself as a “stablecoin of stablecoins” and is backed by Yzi Labs. The protocol converts DEX liquidity positions built from stablecoins into a single stablecoin-like asset, functioning in a similar way to turning an earn vault into an on-chain traded fund.

Its core product, USD*, represents an LP token backed by a basket of stablecoins, including USDC, USDT, and PYUSD, and is conceptually similar to Curve’s former 3pool and 4pool structures. Yield for USD* holders comes primarily from swap fees generated by trading activity within the underlying liquidity pools.

Solstice

Solstice is a Solana-native protocol that issues a delta-neutral stablecoin called USX. Its architecture closely resembles Ethena’s model, with the system split into USX and eUSX. The project is backed by Deus X Capital, which initially committed $100 million in TVL, and current total value locked is around $315 million.

USX

USX functions as the core stablecoin. The official APY displayed on Solstice’s website is 4.4%. On Exponent, a Pendle-style protocol on Solana, the implied YT yield is approximately 16.64%, largely driven by aggressive points and incentive subsidies attached to USX rather than purely organic yield.

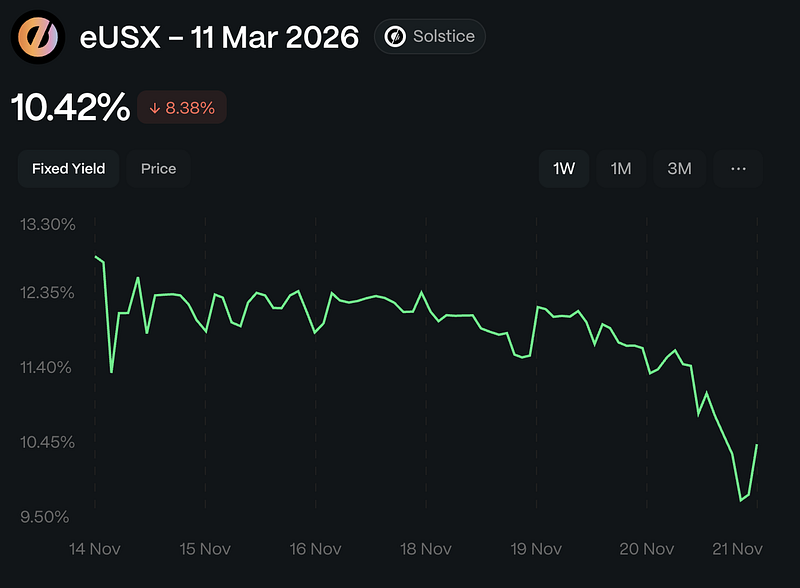

eUSX

eUSX represents the yield-bearing side of Solstice’s dual-token structure. The official APY displayed on the website is 18%. On Exponent, the implied YT yield is approximately 10%.

Disclaimer

This article is published for informational and research purposes only. Any discussion of projects, tokens, or protocols is intended to illustrate broader market trends and does not constitute financial, investment, or legal advice. References to third-party projects are not endorsements, partnerships, or affiliations with Lorenzo Protocol. Readers should conduct their own due diligence and exercise caution when engaging with any project or platform mentioned. Lorenzo Protocol makes no representations or warranties regarding the accuracy, completeness, or reliability of information contained herein, and assumes no liability for any losses or damages arising from its use.